MegaETH's Pre-Deposit Bridge Failed in 156 Seconds. Here's What Went Wrong.

The Setup

MegaETH entered 2025 as one of the most anticipated Ethereum Layer 2 projects in existence. Backed by Vitalik Buterin and Joseph Lubin, with a $20M seed round led by Dragonfly Capital, it promised something the L2 market hadn't delivered: real-time blockchain performance. Sub-millisecond latency. 100,000 TPS. The pitch was that on-chain applications should feel like fast web servers, not clunky settlement layers.

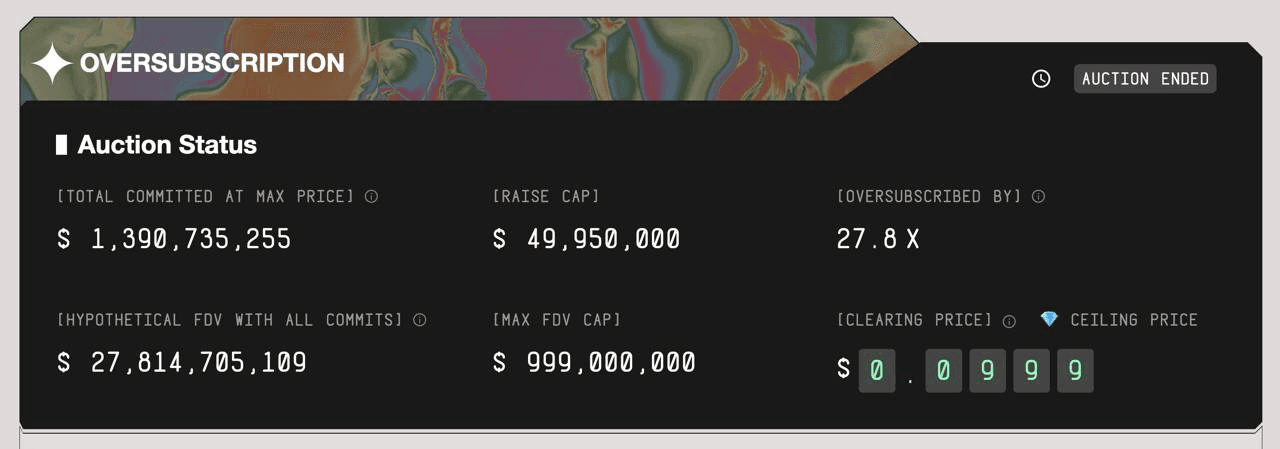

The community believed it. When MegaETH ran its public token sale on Sonar (Echo's KYC platform) in late October 2025, it attracted over 50,000 bidders who collectively committed $1.39 billion — a 27.8x oversubscription against the $49.95M raise cap. Only ~5,000 participants were ultimately selected. The demand signal was deafening.

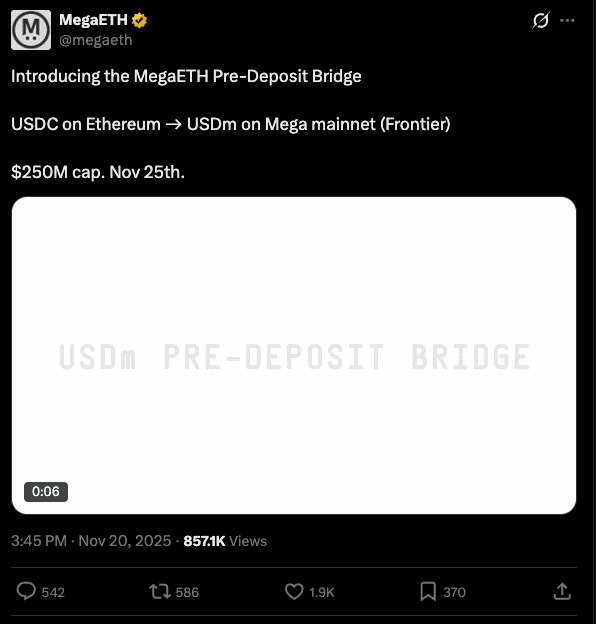

So when MegaETH announced its pre-deposit bridge on November 20, 2025, the expectation was clear: this would be another oversubscribed event for a project with massive demand and institutional credibility.

What actually happened was a masterclass in how not to run a capital formation event.

The Campaign Architecture

MegaETH's pre-deposit bridge was designed to bootstrap USDm — the chain's native stablecoin built with Ethena — ahead of mainnet. Users would deposit USDC on Ethereum and receive USDm on MegaETH's Frontier (pre-mainnet environment), with 2.5% of total MEGA token supply allocated as incentives.

The system had three components:

- The Pre-Deposit Website — operated by MegaETH, handling the user-facing deposit flow and sending KYC validation requests to Sonar.

- The Pre-Deposit Contract — operated by MegaETH via a Safe multisig (4/6 threshold), controlling sale timing, cap limits, and the Sonar sale identifier. Deposits required a valid signature from the website — no direct contract interaction or botting was possible.

- Sonar (by Echo) — the third-party KYC layer, responsible for verifying participant identity before allowing deposits.

Initial cap: $250M. Deposit window: open until either the cap was hit or mainnet (Frontier) launched.

On paper, this is a reasonable setup. In practice, every layer failed simultaneously.

November 25, 2025: The 156-Second Collapse

KYC chaos begins (T-minus 60 minutes)

Sonar verification opened one hour before deposits went live. Immediately: stalled sessions, CAPTCHA loops, inconsistent approval times. Some users cleared KYC in minutes. Others were stuck indefinitely. The verification layer — the only thing standing between participants and the deposit contract — was buckling under load before a single dollar had moved.

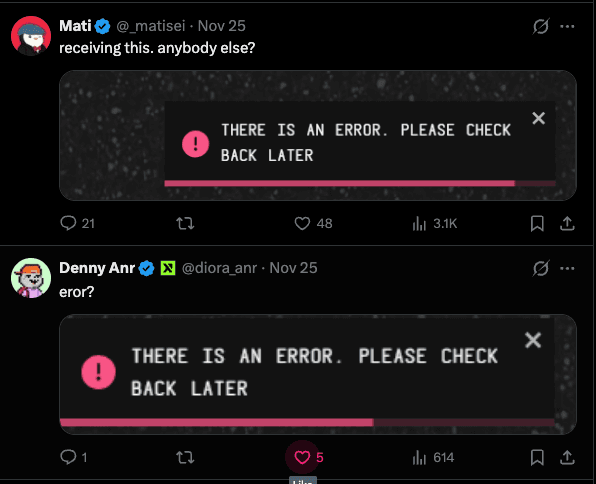

Deposits open, infrastructure breaks (T-zero)

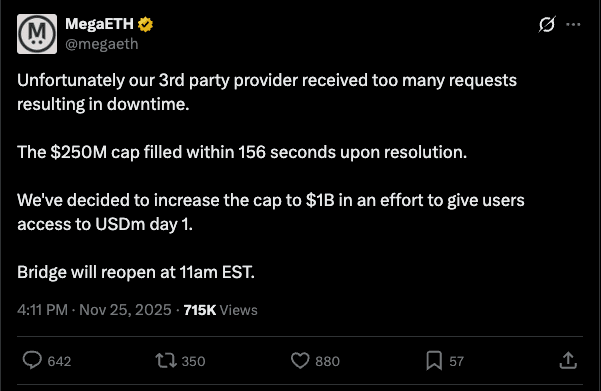

When the pre-deposit bridge went live, the $250M cap filled in 156 seconds.

But "filled" understates what happened. The experience for most participants was not a successful deposit — it was a cascade of errors. Deposits stuck in pending states. UI elements failed silently. Users reported USDC debited from wallets without appearing on the dashboard. Error messages told participants to "check back later" while the cap was being consumed by the wallets that got through.

The wallet cap problem

There was no per-wallet deposit limit.

This meant that while thousands of users fought through broken KYC and failing UI, a handful of large wallets consumed the majority of the allocation. The top 10 deposits accounted for over 30% of total deposits. The single largest deposit: $40M from one address. The second largest: $25.5M from a known whale account (CBB).

Users who missed out — many of whom had been verified and ready — were watching the cap close in real-time while whales with faster infrastructure captured disproportionate allocations. The comment sections turned from excitement to real-time incident reporting.

The cap raise: from $250M to $1B

MegaETH's response to the 156-second fill and the wave of excluded participants was to increase the cap to $1B, announcing a bridge reopen at 11am EST.

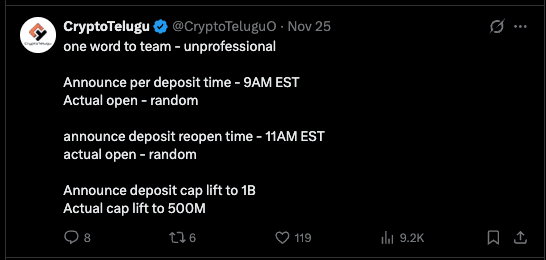

The community reaction was immediate and negative. Users who had deposited at $250M accused the team of diluting early participants by changing terms mid-event. Those who missed the first window questioned whether the reopened bridge would work any better. The communication felt reactive, not planned.

The halt

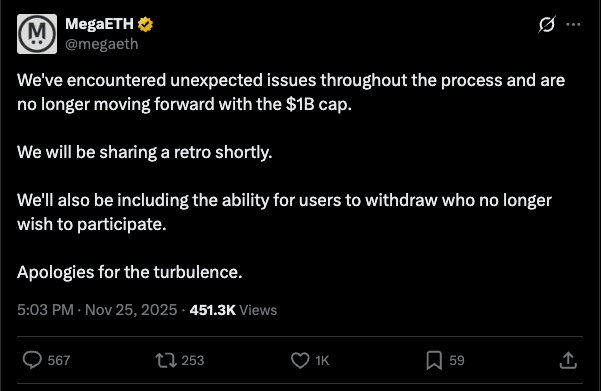

The $1B cap raise never completed. After continued technical issues, MegaETH halted the process entirely, announcing they would share a retrospective.

The retro was published the same day. It acknowledged compounded technical issues but didn't fully satisfy participants. Core complaints remained: multisig execution problems, the sequence of cap changes felt arbitrary, and the lack of per-wallet caps had concentrated deposits among whales.

The refund

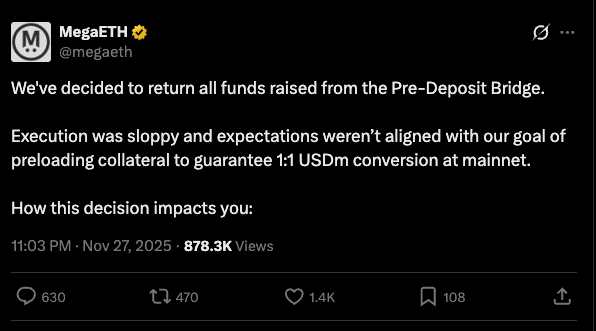

Two days later, on November 27, MegaETH announced full refunds for all pre-deposit bridge participants. The campaign was dead.

The team's own statement was blunt: execution was sloppy. Expectations were misaligned with the goal of preloading collateral for 1:1 USDm conversion at mainnet.

What Actually Failed

This wasn't a single point of failure. It was a systems-level collapse across infrastructure, process design, and communication.

1. Third-party KYC dependency with no load testing

Sonar was a newly launched platform handling its first high-demand event at MegaETH scale. When thousands of users hit it simultaneously, it couldn't keep up. The deposit contract required a valid Sonar signature, which means KYC failures didn't just block users from verifying — they blocked them from depositing entirely, even if they'd already been verified in a prior step.

Building a time-sensitive capital formation event on top of a third-party KYC layer that hasn't been stress-tested at scale is an infrastructure risk that should have been identified in advance.

2. No per-wallet caps

The absence of deposit limits per wallet is the single most consequential design failure. In a capped raise with massive oversubscription (recall: the token sale was 27.8x oversubscribed), no per-wallet cap means the fastest and largest wallets capture the entire allocation.

This isn't theoretical. It's exactly what happened. Ten addresses took 30%+ of the raise. One address took $40M. The result was a pre-deposit event that functionally excluded the retail community it was designed to onboard.

Per-wallet caps are table stakes in any serious capital formation event. They exist to ensure breadth of participation, prevent concentration risk, and maintain community trust. Their absence here was a basic design oversight.

3. Multisig coordination failure

The pre-deposit contract was operated via a 4/6 Safe multisig. When rapid parameter changes were needed — adjusting cap limits, pausing and restarting the bridge — the multisig became a bottleneck. Transactions required coordination among multiple signers under real-time pressure, and the execution was not clean.

For events where decisions must be made in seconds, operational procedures around multisig execution need to be rehearsed and documented. This is not just a technical problem — it's an operational readiness problem.

4. Mid-event parameter changes without pre-communicated contingency

Raising the cap from $250M to $1B mid-event, without a pre-announced escalation path, reads as improvisation under pressure. Even if the decision was defensible on its merits (accommodate more demand), the execution created a trust deficit.

The fix is simple: publish contingency rules before the event starts. "If the cap fills within X minutes, we may expand to Y with Z conditions" gives participants a framework. Announcing it live, after the initial cap has already been consumed, invites the perception of moving goalposts.

5. No staging or pilot phase

A $250M cap raise with tens of thousands of expected participants should not be the first live test of the end-to-end system. A limited pilot — smaller cap, restricted participant set, 24–48 hours before the main event — would have surfaced every issue that ultimately killed the campaign: KYC bottlenecks, UI failures, multisig coordination gaps, and wallet concentration dynamics.

The Aftermath: Mainnet Without a Pre-Deposit Base

MegaETH launched its public mainnet on February 9, 2026 — without the liquidity foundation the pre-deposit bridge was supposed to provide.

Current state (as of early March 2026): TVL sits around $84M. The chain has Aave, Chainlink, and a handful of early DeFi protocols deployed. But the TGE for MEGA hasn't happened yet — it's gated behind three KPI conditions (any one of which triggers TGE, with the event occurring 7 days after the condition is met):

- $500M in circulating USDm (30-day TWAP, with 25%+ in verified smart contracts)

- Ten Mega Mafia apps fully deployed with real usage (100K+ transactions across 25K+ wallets)

- Three dApps generating $50K+ in daily fees for 30 consecutive days

As of early March, none of these conditions have been met. The Mafia app tracker shows 5 of 10 apps live with verified contracts. Top dApp daily fees remain below the $50K threshold. Prediction markets assign ~67% probability to a TGE before June 30, 2026.

The pre-deposit bridge failure didn't kill MegaETH. But it removed a significant liquidity bootstrapping mechanism from the launch playbook. Instead of arriving on mainnet with $250M–$1B in committed stablecoin capital and an engaged depositor base, MegaETH launched from a cold start.

Whether that matters long-term depends on what happens post-TGE — which is why this story will get a second chapter.

What This Tells Us About Pre-Deposit Infrastructure

The MegaETH case is not a story about pre-deposits being broken. Pre-deposits work. Ink, Aptos, Plasma, and dozens of other campaigns have used pre-deposit vaults to successfully bootstrap launch-day liquidity. The primitive is sound.

What MegaETH demonstrates is that execution infrastructure is not optional. A pre-deposit campaign is a capital markets event. It requires the same operational rigor as any structured raise: tested systems, defined allocation rules, contingency planning, and professional coordination.

Specifically, MegaETH's failure reinforces several design principles:

- Per-wallet caps prevent concentration and preserve community trust. Without them, you're running an unstructured first-come-first-served race that rewards infrastructure advantages over genuine participation.

- Third-party dependencies must be stress-tested at expected load. If your deposit flow depends on a third-party KYC layer, that layer needs to perform under 10x your expected concurrent user count, not just average conditions.

- Multisig operations for time-critical events require rehearsal. Parameter changes during a live raise cannot be ad-hoc. The signing flow, contingency triggers, and communication chain should be drilled before the event goes live.

- Contingency rules should be published before the event, not improvised during it. Cap escalation paths, pause conditions, and refund mechanics are trust infrastructure. They need to be visible to participants before they commit capital.

- Staging matters. A limited pilot with a subset of participants and a fraction of the target cap would have caught every issue that ultimately required a full campaign refund.

These are not novel insights. They're standard operating procedure for anyone who has run a structured capital formation event at scale. The fact that a project with $450M+ raised, Vitalik Buterin as a backer, and 50,000+ sale participants still got this wrong underscores the gap between fundraising capability and operational execution in crypto.

What's Next

MegaETH's mainnet is live. The TGE is pending. Once MEGA tokens distribute and the 90-day clock starts, there's a real analysis to be done — TVL trajectories, stablecoin flows, protocol concentration, token price dynamics, and cost of liquidity.

The question for MegaETH is whether a project with this level of backing and community demand can overcome a botched pre-deposit, a cold-start mainnet, and a bear market TGE window to deliver durable liquidity. The data will tell us.

Follow @maxyamp for the follow-up.