Why Pre-Deposits Will Replace Points as DeFi's Default GTM

Points Worked. Then They Didn't.

Between 2023 and 2024, points programs and retroactive airdrops became the dominant go-to-market playbook for every new chain, protocol, and DeFi primitive. The mechanic was simple: promise future tokens, attract deposits, screenshot your TVL chart, tweet about it, raise the next round.

The top five airdrops of 2024 alone distributed over $19 billion in tokens at peak valuations. Across the full year, the number exceeded $26 billion if you include the long tail. An entire cottage industry of airdrop farmers, multi-wallet operators, and Sybil networks emerged to extract value from these programs.

And it worked — for a while. Chains hit headline TVL numbers. Protocols had their "look at this chart" moment. VCs got their markup.

Then the deposits left.

The Graveyard of Rented Liquidity

The data is now in, and it's brutal.

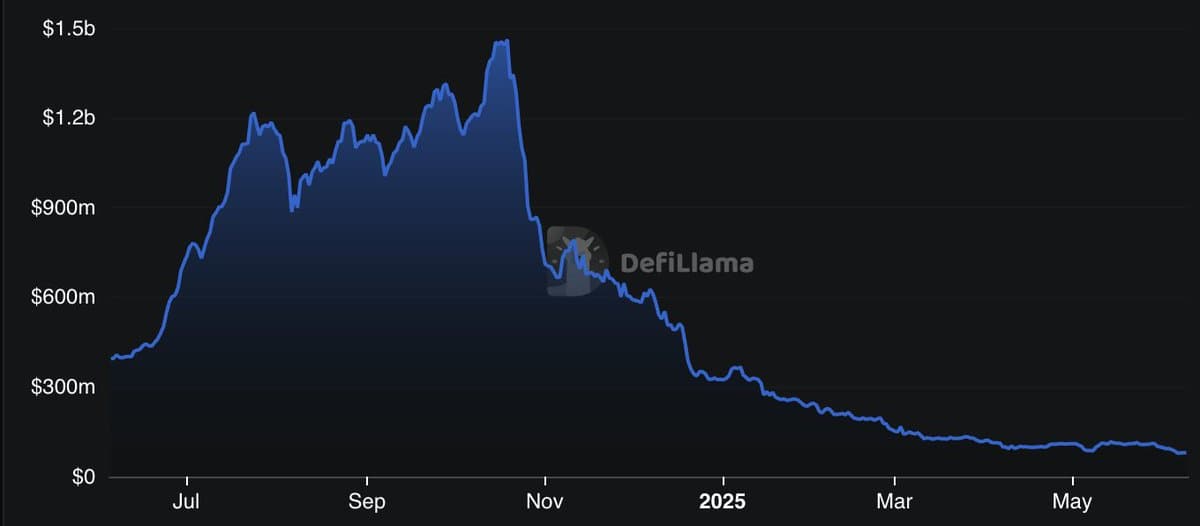

Blast peaked at $3.2 billion in TVL in June 2024, one month before its token launch. Within two months of the airdrop, 60% of that TVL was gone. Today, Blast sits at roughly $35 million — a 98% decline from peak. Daily active users collapsed from 77,000 to 3,500. The BLAST token itself has lost over 90% of its value since listing. The project's official X account went inactive in mid-2025.

zkSync distributed 3.67 billion ZK tokens to nearly 700,000 wallets. The result? Daily active addresses dropped 66% within weeks. TVL contracted to $96 million — its lowest since April 2023. The anticipated engagement boost from the airdrop never materialized.

Starknet saw its TVL in ETH terms decline by more than 50% after its February 2024 airdrop, falling from 456,000 ETH to under 212,000 ETH by July. Daily active addresses dropped below 10,000 — far behind competitors. Its "DeFi Spring" incentive program, designed to re-attract users, failed to reverse the trend.

Scroll saw its TVL surge from sub $500–600 million to more than $1 billion in the days before its airdrop snapshot — then watched ±$300 million evaporate within 48 hours of the snapshot. Transactions dropped 70% in a single day. Key protocols on Scroll lost 16–54% of their individual TVL post-snapshot.

These are not edge cases. According to aggregate data from CoinLaw's 2025 airdrop statistics report, 88% of airdropped tokens lose value within 90 days of distribution. User activity post-airdrop reverts to only 20–40% above pre-airdrop baselines within weeks. The "engagement" was never real — it was a series of transactions performed to qualify for a payout, then abandoned.

The industry spent billions of dollars to rent capital that was never going to stay.

The Real Cost Nobody Talks About

Here's the math nobody does.

A chain launches with a points program. Over six months, it accumulates $500 million in TVL. It allocates 10% of its token supply — call it $200 million at FDV — as incentives to those depositors. Headline: "We bootstrapped half a billion in TVL."

Now check back at Day 90 post-TGE. If the standard pattern holds, 60–80% of that TVL is gone. The remaining capital is perhaps $100–150 million. But the team has already spent $200 million in token emissions to acquire it. The effective cost? Somewhere between $1.30 and $2.00 per dollar of TVL that actually stuck around for three months.

And that's before you factor in the secondary effects: the token selling pressure from farmers dumping their allocation (the median claim-to-sell time for airdrop recipients is measured in hours, not days), the reputational damage from community backlash over "unfair" distributions, and the demoralization of actual users who get diluted by professional multi-wallet operators.

The industry optimizes for the wrong metric. Peak TVL is a vanity number. What matters is TVL-days — how much capital stayed, for how long. A protocol with $50 million that stays for a year is more valuable than $500 million that leaves after a week. But nobody measures it that way, so nobody optimizes for it.

What Pre-Deposit Vaults Actually Solve

A pre-deposit vault is a structurally different primitive. Instead of "do things on our chain and maybe we'll give you tokens later," it's "here are the exact terms — APY, lockup, vesting, risk parameters — commit your capital upfront, and we deploy it on Day 1."

This changes the incentive structure from the ground up.

For Chains and Protocols

-

Day-1 liquidity, not Day-1 farming. When a new chain or lending market goes live, the pre-deposit vault already has committed capital waiting to deploy. There is no cold-start problem. Lending markets open with borrowable liquidity. DEXs launch with pool depth. Users arrive to a functioning ecosystem, not an empty shell waiting for TVL to trickle in.

-

Demand signal before resource commitment. A pre-deposit campaign tells you, before launch, exactly how much capital the market is willing to commit to your ecosystem at your proposed terms. That's real information — the difference between building a venue and hoping people show up, versus taking reservations first.

-

Better unit economics. Instead of spraying tokens across thousands of unknown wallets hoping some of the capital sticks, you negotiate specific terms with identified counterparties. You know who your LPs are. You know their ticket size, their expected hold period, their history. The cost per retained TVL-day is structurally lower because you're not paying for the 80% that was always going to leave.

-

A marketing event, not just a financial one. A well-structured pre-deposit campaign — "$75 million committed before mainnet" — generates genuine narrative momentum. It's a signal of institutional confidence that attracts developers, other protocols, and organic users. It compounds in a way that a points leaderboard never does.

For LPs

-

Known terms, not vague promises. "Deposit now, we'll figure out rewards later" is what got us into this mess. A pre-deposit vault says: here's the base yield, here's the token incentive (at what FDV, with what vesting), here's the lockup (with what exit mechanics), and here's the risk profile. LPs can underwrite the opportunity the way institutional allocators underwrite any deal — with a term sheet.

-

Reduced information asymmetry. In a points program, nobody knows the conversion ratio until after the fact. LPs are betting blind. In a pre-deposit structure, the terms are explicit. This doesn't eliminate risk, but it moves the risk from "will they screw us on the distribution?" to "will the protocol execute on its roadmap?" — which is at least a productive risk to take.

-

Skin in the game on both sides. When a protocol commits to specific terms in a pre-deposit vault — a guaranteed APY floor, a fixed FDV for token incentives, a defined lockup with fair exit — they're making a binding commitment. They can't retroactively change the rules. This creates accountability that points programs fundamentally lack.

Anatomy of a Well-Structured Pre-Deposit

Not all pre-deposits are created equal. Here's what separates a good program from a sloppy one.

- Clear capacity caps. Open-ended programs attract unlimited low-quality capital. The best pre-deposits set a hard cap ($3–75 million is a common range), which forces selectivity and creates urgency.

- Transparent APY composition. "Up to 60% APY" is meaningless without a breakdown. Good structures decompose yield into layers: base yield (real, sustainable), token incentives (at a stated FDV, with defined vesting), and optional boosts. Each layer has different risk characteristics.

- Defined lockup with fair exit. A soft lock — where withdrawing early forfeits incentives but returns principal — is fair. The best programs tier their lockup mechanics: you can leave, but the longer you stay, the better your terms.

- Security posture. At a minimum: third-party audit of the vault contracts, transparent admin key structure, defined emergency procedures, and clearly documented withdrawal mechanics. Unaudited vaults with opaque admin controls are a non-starter for institutional capital.

- Curator accountability. In multi-vault setups, somebody has to own the allocation decisions. That curator needs clear terms of reference: venue allow/deny lists, concentration caps, rebalance triggers, reporting cadence.

Where This Goes

The trajectory is clear if you squint.

Pre-deposit vaults are right now where token launches were in 2017 — bespoke, manually coordinated, relationship-driven. Every deal is custom. Every term sheet is negotiated from scratch. The operational overhead is high, which limits it to larger programs.

But the demand side is exploding. There are now over 100 L2s deployed on Ethereum alone, per L2Beat's data. Every new chain needs liquidity. Every new lending market needs deposits. Every new perp DEX needs vault capital. And the supply of LP attention is finite and getting more fragmented.

The obvious next step is standardization — template-based programs where a new chain defines its parameters (capacity, terms, lockup, asset, network), plugs into existing vault infrastructure and LP distribution networks, and goes live in days instead of months.

Beyond that, the real unlock is retention measurement. The industry desperately needs a shared metric — something like "cost per TVL-day" or "D+30/D+90 retention rate" — that makes liquidity programs comparable and auditable. Until we have that, teams will continue to be judged by screenshots instead of outcomes.

The pre-deposit vault is the first primitive that gets this right by design. By defining terms upfront, committing capital before launch, and measuring retention through lockup mechanics, it structurally selects for the kind of capital that chains and protocols actually need.

Points gave us the screenshot era. Pre-deposits give us the underwriting era. It's time to stop renting liquidity and start structuring it.